I couldn’t have picked a better day to write about the OIH getting cheaper than yesterday! To be fair I got lucky on the timing. The OIH and the rest of the energy complex simply marked losses in the broader indexes, which took their cue from the strange bed fellows of Greenspan (2H07 recession a possibility) and the Chinese (reigning in growth) – both factors that will reduce hydrocarbon demand.

Oil Was Remarkably Resilient Into The Close Of Nymex Trading… April crude closed up $0.07 at $61.46 in a wild day of trading.

…But When The Dow Took A Header Around 2:30 EST, The USO ETF Started To Trade Off Sharply. No doubt hedge funds heading for the exits. Electronic trading saw NYMEX oil reverse course before the close of stock trading, easily tumbling through $61 as the possible global deceleration and its potential impact on oil demand and prices began to be felt.

Recent demand growth prognostications now in question. From the IEA’s January Oil Market Report dated two weeks ago: Global oil product demand is raised by 111 kb/d in 2006 to 84.5 mb/d and by 273 kb/d in 2007 to 86.0 mb/d following revisions to China. They may have to trim this back some.

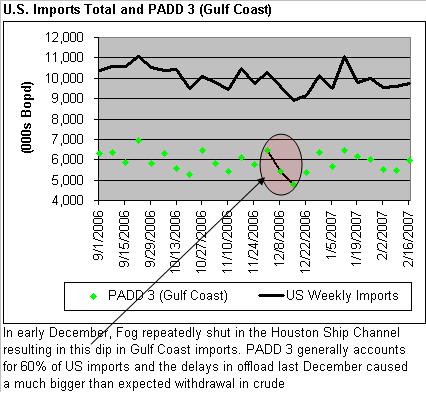

Oil Inventory Day: Analysts and Traders Are Looking For More Large Product Draws And A Small Build In Crude. As I mentioned yesterday, the Houston Ship Channel (HSC) was shut down due to dense fog beginning last Thursday and appears to have remained shut through Friday, the last day of the oil inventory reporting period. This is temporary and in my mind provides bears with a sort of “get of jail free” pass. By this I mean seemingly bullish numbers (unless they are vastly out of line with expectations) can be dismissed like non-recurring items on an income statement.

Oil Inventory Expectations (from the Reuters survey) :

- Crude Oil: Up 1.9 million barrels. The change in crude inventories could easily be lower than Street expectations due to the partial week closure of the HSC and potentially could be a small draw on inventories.

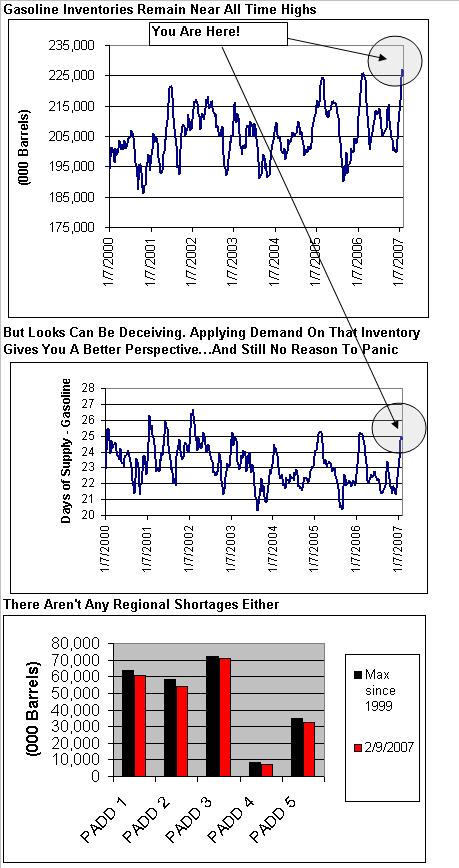

- From the beginning of December to the middle of the month crude imports fell by roughly 1.6 mm bopd or 11 mm barrels per week through the Gulf Coast. Then analysts “expected” a draw of only 1.7 mm barrels but got blindsided by a drop of over 6 mm barrels. That’s a long winded way of saying that today’s number could even be a draw on crude supplies as could next week’s report. It all depends on the duration of the closure. However, as always “this too shall pass” and the U.S. remains exceedingly well stocked as seen below:

- Gasoline: Down 1.8 million barrels. With all the refinery outages and an increasing number of local shortages gasoline is moving towards center stage as a key determinant of oil prices. Blending component consumption could easily make this number larger than this which would lend support to crude prices on a normal day. I think the amount of fear in the market will require a much bigger draw than the 1.8 mm barrel expectation to rally/support crude.

- Distillate: Down 2.8 million barrels. I think this is probably a bit light but I’m not sure a “low ball” miss here will prompt much of a rally (at least much of a sustainable one) in heating oil or crude oil this late in the heating season.

Odds & Ends

Natural Gas has been quietly trading lower on the expectation that this week’s inventory report will show a withdrawal somewhere in the neighborhood of half of last week’s pull from storage. Gas sliced through $7.50 overnight and, barring any surprises tomorrow, could be headed towards a test of $7 by the weekend as inventories continue to track towards a seasonal trough of 1.4 Tcf. More on gas in tomorrow’s post.

Spring Is On The Way. The weather “will turn very warm for much of the area that had one of the coldest Februaries on record,” said Joe Bastardi, lead forecaster at AccuWeather in State College, Pennsylvania.~Bloomberg

Opec Watch: Iran says it will “never” stop uranium enrichment, no doubt in a bid to ease tensions and lower oil prices for everyone. Admed’s trying to enrich something all right and not just uranium. Check here for all the latest Iran facts, figures, and er, um critiques.

Analyst Watch: nada.

Putin Watch: Gazprom lowers Rospan’s gas volume transportation allowance in a move critics say is more strong arm tactics designed to force a sale of the TNK-BP venture.

Holdings Watch:

- Small BHI and SLB positions remain ontrack posting nice retrenchments on the day,

- BP puts came back to life after the settlement party of the prior two days was abruptly cut short by the group’s retrenchment,

- sold my XOM position bought at $1.25 over the last 10 days for $1.75 and thought I was lucky to have escaped (that was before the Dow plummetted 200 points while I grabbed a Coke and the $75 March put I had just sold went on to close at $3.30 bid!!! (kick, kick, kick)),

- shied away from any more TSO puts although they reversed hard with everything else. They and VLO may be reasonable shorts going forward as gasoline prices should begin to sort themselves out (that’s code for fall) in the next few weeks as a number of snafu are fixed and refinery utilization slowly climbs out of its current maintenance season induced lull of 85%,

- Picked up a small put position on PTR (March 110s for $1.30 near the close) – a rank wildcat of a trade on the sincere belief that their will be further follow through in the morning on yesterday’s weakness. The better decision was to avoid the temptation to play the early bounce in the market and the group which was brief and would have been very painful,

- HES – the insider selling continues and although the stock fell 4% yesterday it was essentially in line with it’s peers and remains near record highs. I have not yet seen the catalyst (other than substantially lower oil) that can put a real dent in the shares.

{kind=link}

{kind=link}

{kind=link}

{kind=link}